Two Decades, Two Journeys

Imagine two people standing at different points in life. One is 25, just stepping into financial independence with a hopeful heart and ambitious dreams. The other is 45, seasoned by experience and likely juggling career goals, a family, and long-term plans. They both want to invest. But how they approach it, what drives them, and the risks they can take differ significantly.

Investing is not a one size fits all. Your age, responsibilities, mindset, and tolerance for risk shape your financial journey. Whether you are just starting or working hard to secure the future, understanding how investing differs in your 20s versus your 40s can guide your next steps more wisely.

Let us explore what sets these decades apart and how to make the most of your investments no matter your age.

1. Time Horizon: The Magic of Time Versus the Power of Urgency

When you are in your 20s, time is on your side. You can afford to let investments sit and grow for decades. Compounding becomes your secret weapon. For example, investing just $200 per month at an average return of 7 percent starting at age 25 can grow to over $500,000 by age 65.

In your 40s, you still have time, but not as much. You may have 20 years until retirement rather than 40. That means you may need to invest more aggressively in terms of amount, not necessarily in risk, to catch up or reach your goals.

What this means in practice:

In your 20s: Prioritize consistency over perfection. Time will do much of the heavy lifting for you.

In your 40s: You need a sense of urgency. Focus on maxing out contributions and avoid any delay in getting started.

2. Risk Appetite: Bold Beginnings Versus Measured Moves

In your 20s, the stakes feel lower. If an investment goes south, there is time to recover. That is why younger investors often lean toward higher-risk assets like growth stocks, tech companies, and even cryptocurrencies.

In your 40s, risk tolerance typically declines. You may be more concerned with preserving capital than chasing high returns. That does not mean avoiding stocks altogether, but it does mean striking a better balance between risk and stability.

In your 20s: You can afford to be adventurous. A well-diversified, stock-heavy portfolio might make sense.

In your 40s: Caution is wise, but so is balance. Include bonds, real estate, or dividend-paying stocks for steadier returns.

3. Income, Lifestyle, and Financial Responsibilities

Your financial obligations change dramatically between your 20s and 40s. When you are younger, you might earn less, but your responsibilities are minimal. You might not yet have a mortgage, a spouse, or children. That gives you room to save and invest more freely, even if in smaller amounts.

In your 40s, you likely earn more but have higher financial demands. Between kids, education costs, mortgage payments, insurance, and retirement planning, it can feel like your money is being pulled in several directions.

What this means for investing:

In your 20s: Save aggressively when possible. Living frugally now can lead to greater financial flexibility later.

In your 40s, Budgeting becomes crucial. You must invest smartly around existing obligations, possibly automating investments to stay on track.

4. Investment Vehicles: What Tools Are Right for Each Decade

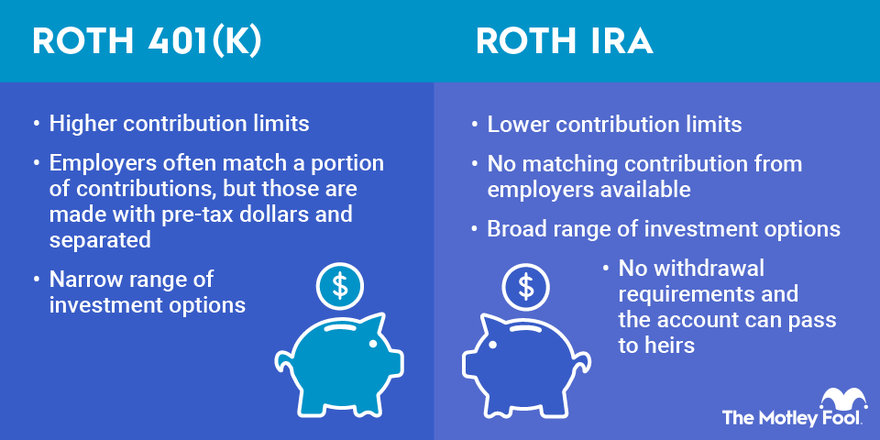

In your 20s, simplicity and accessibility matter. You may be using employer-sponsored retirement accounts like a 401k or starting a Roth IRA. Robo-advisors and index funds offer a great way to begin without needing advanced knowledge.

In your 40s, your strategy often becomes more diversified and sophisticated. You might be contributing to multiple retirement accounts, investing in real estate, or starting to look into tax minimization strategies.

Tools to explore in your 20s:

Roth IRA

Index funds and ETFs

Fractional shares

Robo-advisor platforms

Tools to explore in your 40s:

401 (k) with matching

Real estate for passive income

Brokerage accounts for dividend investing

College savings plans like 529s

Health savings accounts with investment options

5. Financial Goals and Life Priorities

Goals evolve with age. In your 20s, your financial priorities may include paying off student debt, building an emergency fund, or saving for a vacation. These are important goals, but they are often shorter-term and more lifestyle-oriented.

In your 40s, long-term security takes center stage. You might be focused on retirement planning, college tuition, buying a second home, or estate planning.

In your 20s: It is the ideal time to experiment and define what financial freedom looks like to you.

In your 40s: The vision becomes clearer. It is about staying on track and aligning your investments with upcoming needs.

6. Emotional Landscape: Confidence, Fear, and Course Correction

Money decisions are never just about numbers. Emotions run deep in both decades, but they take different forms.

In your 20s, you might face peer pressure or get swept up in hype, especially with financial trends going viral online. It is easy to make impulsive investment decisions driven by fear of missing out or social comparison.

In your 40s, emotion can manifest as regret, wishing you had started earlier or done things differently. But that is also where clarity and discipline enter. You have lived through enough cycles to know that slow and steady wins the race.

In your 20s: Learn to separate emotion from action. Do not chase returns. Stay consistent.

In your 40s: Focus on realistic, achievable goals. There is still time to build wealth with the right mindset and tools.

7. Mistakes to Avoid in Both Decades

Nobody is immune to missteps, no matter their age. But the nature of those mistakes changes as you grow.

Common mistakes in your 20s:

Waiting too long to start investing

Relying too much on social media for financial advice

Avoiding risk entirely or taking on too much

Neglecting to build financial literacy

Common mistakes in your 40s:

Being overly conservative out of fear

Not adjusting investment strategy as income increases

Failing to plan for taxes or inflation

Prioritizing children’s future at the expense of your retirement

Each age brings its traps, but self-awareness and a little guidance can help you avoid them.

8. The Evolving Portfolio: Adapting With Age

No matter how old you are, investing is not a static game. Your portfolio should evolve as your life does. What you prioritized in your 20s may no longer serve you in your 40s, and that is perfectly natural.

In your 20s: You build. You learn, experiment, and lay foundations.

In your 40s: You refine. You adjust, protect, and optimize what you have built.

Tips for all ages:

Review your portfolio every six to twelve months

Adjust your risk levels with life changes

Rebalance your asset allocation periodically

Stay informed and curious

Investing in Your 20s vs 40s

| Factor | In Your 20s | In Your 40s |

|---|---|---|

| Time Horizon | Long horizon; time to let compounding work. | Shorter horizon; need more planning. |

| Risk Appetite | High risk tolerance; can afford aggressive growth. | Lower risk tolerance; need balance and capital preservation. |

| Income & Responsibilities | Lower income but fewer financial obligations. | Higher income but more financial demands (kids, mortgage, etc.). |

| Investment Tools | Start with Roth IRA, index funds, and robo-advisors. | Use 401k, real estate, brokerage accounts, HSA, and tax strategies. |

| Financial Goals | Pay debt, build an emergency fund, and save for travel or big purchases. | Focus on retirement, college funds, and estate planning. |

| Emotional Landscape | FOMO, peer pressure, chasing hype. | Regret, discipline, long-term clarity. |

| Common Mistakes | Waiting too long, relying on social media, taking too much or too little risk. | Being overly conservative, neglecting tax planning, and focusing only on kids. |

| Portfolio Strategy | Build and experiment; lean into learning. | Refine, rebalance, and protect what you’ve built. |

There Is No Late, Only Next

Whether you are starting at 25 or 45, the most important decision is to start. The idea that you are behind is a myth. You are where you are, and your journey forward is all that matters now.

In your 20s, you have time. In your 40s, you have wisdom. Both are powerful. Use what you have, stay consistent, and invest with intention. The future favors the focused.